Sunland Diesel owns the Fredonia Barber Shop. He employs 4 barbers and pays each a base rate of $1,440 per month. One of the barbers serves as the manager and receives an extra $520 per month. In addition to the base rate, each barber also receives a commission of $9.15 per haircut. Other costs are as follows.

Advertising $240 per month

Rent $1,100 per month

Barber supplies $0.35 per haircut

Utilities $185 per month plus $0.10 per haircut

Magazines $35 per month Sunland currently charges $16 per haircut.

Vin currently charges $10 per haircut.

Required:

a. Determine the variable costs per haircut and the total monthly fixed costs.

b. Compute the break-even point in units and dollars.

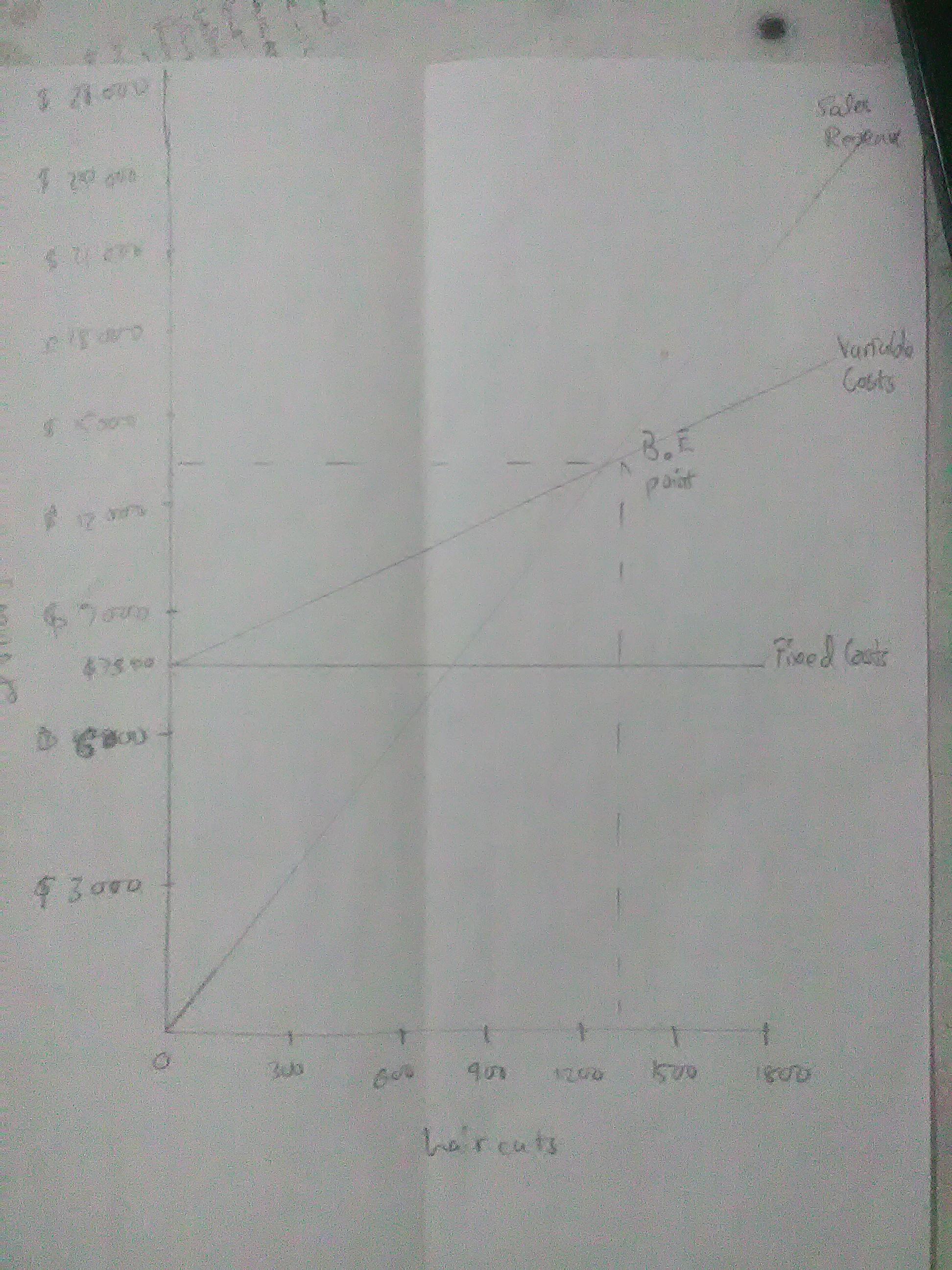

c. Prepare a CVP graph, assuming a maximum of 1,800 haircuts in a month. Use increments of 300 haircuts on the horizontal axis and $3,000 on the vertical axis.

d. Determine net income, assuming 1,600 haircuts are given in a month.

Answers

Answer:

a. Variable costs = $9.60 and Fixed Costs = $7,840

b. 1,225 haircuts and $19,600

c. See attachment

d. $2,400

Explanation:

Variable Costs per haircut Calculations

Barber supplies $0.35

Utilities $0.10

Commission $9.15

Total Variable Costs per haircut $9.60

Total Monthly Fixed Costs Calculation

Base Salary (1,440 × 4 + 520) $6,280

Advertising $240

Rent $1,100

Utilities $185

Magazines $35

Total Monthly Fixed Costs $7,840

Contribution per unit = Selling price per unit - Variable Cost per unit

= $16.00 - $9.60

= $6.40

Contribution Margin Ratio = Contribution ÷ Selling Price

= $6.40 ÷ $16.00

= 0.40

Break-even point (units) = Fixed Cost ÷ Contribution per unit

= $7,840 ÷ $6.40

= 1,225 haircuts

Break-even point (dollars) = Fixed Cost ÷ Contribution Margin Ratio

= $7,840 ÷ 0.40

= $19,600

Net income, assuming 1,600 haircuts are given in a month [calculation]

Contribution (1,600 × $6.40) $10,240

Less Fixed Costs ($7,840)

Net Income/(loss) $2,400

Related Questions

Last week, an investigative reporter for a major metropolitan newspaper discovered that the doctors conducting clinical trials of a new cancer treatment drug are also the principal shareholders in Cancer Solutions Inc. (CSI). CSI is the company developing and attempting to market the drug. Upon being interviewed by federal authorities, the doctors acknowledged their conflict of interest but reported that they were sold the shares at a 75% discount by CSI's chief financial officer. The CFO was concerned that CSI might not be able to meet its annual performance objectives and in turn pay his anticipated multimillion-dollar bonus.

Does an agency conflict exist between CSI's CFO and the company's shareholders?

a. Yes; CSI's CFO engaged in unethical conduct to manipulate the firm's short-term earnings and improve the likelihood of receiving his annual bonus.

b. Yes; the shares should not have been sold at a 75% discount, which is price discrimination.

c. No; professionals, such as doctors and professional money managers, would not participate in unethical activities.

d. No; in general, shareholders are satisfied with company officers engaging in any type of legal or illegal activity to ensure the chances of them receiving greater dividend payments.

Which of the following actions will help ease agency conflicts and better align managers' objectives with the firm's shareholder wealth?

a. Pay the manager a combination of salary and stock options (phased in over several years) that reward him or her for consistently increasing shareholder wealth.

b. Pay the manager a large base salary with a huge stock option package that matures on a single date.

Amalgamated Metals Corporation's stockholders are mostly individual investors, and there is relatively little institutional ownership. If several pension and mutual funds were to take large positions in Amalgamated Metals Corporation's stock, direct shareholder intervention would be___________ likely to motivate the firm's management.

Answers

Answer:

FIRST QUESTION

A)Yes; CSI's CFO engaged in unethical conduct to manipulate the firm's short-term earnings and improve the likelihood of receiving his annual bonus.

SECOND QUESTION

A)Pay the manager a combination of salary and stock options (phased in over several years) that reward him or her for consistently increasing shareholder wealth.

LAST QUESTION

MORE likely

Explanation:

We are informed from the question about an investigative reporter for a major metropolitan newspaper discovery about the doctors conducting clinical trials of a new cancer treatment drug are also the principal shareholders in Cancer Solutions Inc. And how The CFO was concerned that CSI might not be able to meet its annual performance objectives and in turn pay his anticipated multimillion-dollar bonus.

In this case there is an agency conflict that exist between CSI's CFO and the company's shareholders, this is because the, CSI's CFO engaged in unethical conduct to manipulate the firm's short-term earnings and improve the likelihood of receiving his annual bonus.

Agency conflict in finance, is also regarded as conflict of interest, usually occur between the management and the shareholders of that company, it is conflict that usually emerge when those that are required for certain responsibility like interest of principal decide to divert the the authority for their own benefits. However,agency conflict can be minimized by allowing transparency and some ways.

It should be noted here that the CSI's CFO engaged in unethical conduct to manipulate the firm's short-term earnings and improve the likelihood of receiving his annual bonus which is the reason behind the conflict because he act on his own interest.

SECOND QUESTION,

Which of the following actions will help ease agency conflicts and better align managers' objectives with the firm's shareholder wealth?

From the explanation of Agency conflict from First question it should be noted that there are some actions that will help to ease agency conflicts and better align managers' objectives with the firm's shareholder wealth such as

Payment of the manager a combination of salary and stock options (phased in over several years) that reward him or her for consistently increasing shareholder wealth.

The payment of the stock options to the manager will allow selling of stock at agreed price as well as date.

LAST QUESTION

Amalgamated Metals Corporation's stockholders are mostly individual investors, and there is relatively little institutional ownership. If several pension and mutual funds were to take large positions in Amalgamated Metals Corporation's stock, direct shareholder intervention would be__MORE__ likely to motivate the firm's management.

Cash flows from operations may not be sufficient for a firm to keep up with growth-related financing needs, or the firm may not be able to always generate enough cash flow to maintain a surplus of cash. Firms prefer to borrow now to fulfill their capital requirements through means of short-term financing or long-term financing. Both methods have their advantages and disadvantages.

The following statement identifies a possible characteristic of short-term financing.

Consider this case:

Short-term loans usually have a lower cost than long-term loans. Identify whether the preceding statement is true or false.

a. This statement is false and a disadvantage of short-term financing.

b. This statement is true and an advantage of short-term financing.

Firms use a variety of short-term financing sources to support working capital. Use the descriptions in the following table to identify the short-term financing source.

Description Short-Term Financing Source

A formal, committed line of credit extended by a bank or other lending institution.

An obligation backed by collateral, often inventories or accounts receivable.

Answers

Answer:

1. Consider this case:

Short-term loans usually have a lower cost than long-term loans. Identify whether the preceding statement is true or false.

a. This statement is false and a disadvantage of short-term financing.

2. Identify the short-term financing source:

An obligation backed by collateral, often inventories or accounts receivable.

Explanation:

Some organizations regularly require short-term financing to ease uneven cash flows. It is also called working capital financing. Its duration is less than 12 months, unlike long-term financing that can last more than two years. Most of this financing is arranged with banks in the form of bank overdraft.

Broca Corporation has a current ratio of 2.5. Which of the following transactions will increase Broca's current ratio? Select one: a. the purchase of inventory for cash. b. the collection of an account receivable. c. the payment of an account payable. d. none of the above.

Answers

Answer:

b. the collection of an account receivable

Explanation:

The formula to compute the current ratio is shown below:

As we know that

Current ratio = Current assets ÷ Current liabilities

If the current ratio is 2.5 that means the current assets is higher than the current ratio

As per the given options, the option b is correct and hence the same is to be considered

The transaction that will increase Broca's current ratio is d. none of the above.

The current ratio is not increased by the purchase of inventory for cash because this transaction has no effect on the current assets. The collection of an account receivable is not going to increase the current ratio for the same reason above (no effect on the current assets).

The payment of an account payable reduces the current assets and current liabilities by the same amount and will not affect the current ratio.

Thus, the transaction that will increase the current ratio is d.

Learn more: https://brainly.com/question/17189534

The following inventory valuation errors have been discovered for Knox Corporation:

The 2015 year-end inventory was overstated by $23,000

The 2016 year-end inventory was understated by $61,000

The 2017 year-end inventory was understated by $17,000

The reported income before taxes for Knox was:

Year: Income before Taxes:

2015 $138,000

2016 $254,000

2017 $168,000

Required:

Compute what income before taxes for 2015, 2016, and 2017 should have been after correcting for the errors.

Answers

Answer:

Income +/- inventory adjustment

2015: 138,000 - 23,000 = 115,000

2016: 254,000 + 61,000 = 315,000

2017: 168,000 + 17,000 = 185,000

Explanation:

Inventory Identity:

Beginning + Purchases = Ending + COGS

As the mistake is on the right side it compensates by the other component which is COGS

When the inventory is overstated this means COGS is understated.

We didn't record the cost of good sold thefore our gross profit is higher making the net income higher.

When the inventory is understated this means COGS is overstated.

We record more cost of goods sold thefore our gross profit is lower making the net income fewer as well.

Question 5 of 10

Why do business often add fees to their invoices?

O A. To help pay for business expenses

B. To attract new customers

C. To reward customers' for their loyalty

D. To make more profit than their competitors

Answers

Answer: I think it's A

Explanation:

Answer:

Its A!

Explanation:

Just took the quiz

On December 31, 2021, the end of the fiscal year, California Microtech Corporation completed the sale of its semiconductor business for $15 million. The semiconductor business segment qualifies as a component of the entity according to GAAP. The book value of the assets of the segment was $13 million. The loss from operations of the segment during 2021 was $4.8 million. Pretax income from continuing operations for the year totaled $7.8 million. The income tax rate is 25%.

Prepare the lower portion of the 2021 income statement beginning with income from continuing operations before income taxes. Ignore EPS disclosures. (Amounts to be deducted and negative amounts should be indicated with a minus sign. Enter your answers in whole dollars and not in millions.)

Answers

Answer and Explanation:

The preparation of the lower portion is presented below:

Income from the continuing operation

before income tax $7,800,000

Less: Income tax expenses ($7,800,000 × 25%) (1,950,000)

Income from continuing operation(A) 5,850,000

Discontinued operation:

Loss from operation discontinued components

($15 - $13 - $4.8) ($2,800,000)

Income tax benefits ($2,800,000 × 25%) $700,000

Loss on discontinued operation(B) ($21,000,000)

Net loss (A - B) -$15,150,000

Thirteen students entered the business program at Sante Fe College 2 years ago. The following table indicates what each student scored on the high school SAT math exam and their grade-point averages (GPAs) after students were in the Sante Fe program for 2 years.

Student A B C D E F G

SAT Score 421 375 585 693 608 392 418

GPA 2.93 2.87 3.03 3.42 3.66 2.91 2.12

Student H I J K L M

SAT Score 484 725 506 613 706 366

GPA 2.50 3.24 1.97 2.73 3.88 1.58

The least-squares regression equation that shows the best relationship between GPA and the SAT score is:________ (round your responses to four decimal places)

Answers

Answer:

ŷ = 0.0035X + 1.0030

Explanation:

Given the data :

Student A B C D E F G H I J K L M

SAT Score: 421 375 585 693 608 392 418 484 725 506 613 706 366

GPA: 2.93 2.87 3.03 3.42 3.66 2.91 2.12 2.50 3.24 1.97 2.73 3.88 1.58

We can obtain the Least square regression calculator, we can obtain the least square regression equation in the Format :

y = mx + c

Where ; m = gradient / slope

x = predictor variable ; c = intercept

y = Independent variable.

The model equation produced by the calculator is :

ŷ = 0.0035X + 1.0030

y predicted variable ; x = explanatory variable

0.0035 = slope or gradient ; 1.0030 = intercept

Find out more information about sat score here:

https://brainly.com/question/2264831

Leach Inc. experienced the following events for the first two years of its operations:

Year 1:

Issued $10,000 of common stock for cash.

Provided $78,000 of services on account.

Provided $36,000 of services and received cash.

Collected $69,000 cash from accounts receivable.

Paid $38,000 of salaries expense for the year.

Adjusted the accounting records to reflect uncollectible accounts expense for the year.

Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Closed the revenue account. Closed the expense account.

Year 2:

Wrote off an uncollectible account for $650.

Provided $88,000 of services on account.

Provided $32,000 of services and collected cash.

Collected $81,000 cash from accounts receivable.

Paid $65,000 of salaries expense for the year.

Adjusted the accounts to reflect uncollectible accounts expense for the year.

Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Required

a. Record the Year 1 and Year 2 events in general journal form and post them to T-accounts.

b. Prepare the income statement, statement of changes in stockholders’ equity, balance sheet, and statement of cash flows for Year 1 and Year 2.

c. What is the net realizable value of the accounts receivable at Year 1 and Year 2?

Answers

Answer:

a.1) year 1

Issued $10,000 of common stock for cash.

Dr cash 10,000

Cr common stock 10,000

Provided $78,000 of services on account.

Dr accounts receivable 78,000

Cr service revenue 78,000

Provided $36,000 of services and received cash.

Dr cash 36,000

Cr service revenue 36,000

Collected $69,000 cash from accounts receivable.

Dr cash 69,000

Cr accounts receivable 69,000

Paid $38,000 of salaries expense for the year.

Dr wages expense 38,000

Cr cash 38,000

Adjusted the accounting records to reflect uncollectible accounts expense for the year. Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Dr bad debt expense 450

Cr accounts receivable 450

Closed the revenue account. Closed the expense account.

Dr service revenue 114,000

Cr income summary 114,000

Dr income summary 38,450

Cr wages expense 38,000

Cr bad debt expense 450

Dr income summary 75,550

Cr retained earnings 75,550

b.1) income statement year 1Service revenue $114,000

Expenses:

Wages $38,000Bad debt $450 ($38,450)Net income $75,550

balance sheet year 1Assets:

Cash $77,000

Accounts receivable $8,550

total assets $85,550

Equity:

Common stock $10,000

Retained earnings $75,550

total equity $85,550

statement of cash flows year 1Cash flows form operating activities:

Net income $75,550

adjustments:

Increase in accounts receivable ($8,550)

net cash from operating activities $67,000

Cash flow from financing activities:

Common stocks issued $10,000

Net cash increase $77,000

beginning cash balance $0

Ending cash balance $87,000

a.2) Year 2:

Wrote off an uncollectible account for $650.

Dr bad debt expense 650

Cr accounts receivable 650

Provided $88,000 of services on account.

Dr accounts receivable 88,000

Cr service revenue 88,000

Provided $32,000 of services and collected cash.

Dr cash 32,000

Cr service revenue 32,000

Collected $81,000 cash from accounts receivable.

Dr cash 81,000

Cr accounts receivable 81,000

Paid $65,000 of salaries expense for the year.

Dr wages expense 65,000

Cr cash 65,000

Adjusted the accounts to reflect uncollectible accounts expense for the year. Leach estimates that 5 percent of the ending accounts receivable balance will be uncollectible.

Dr bad debt expense 745

Cr accounts receivable 745

b.2) income statement year 2Service revenue $120,000

Expenses:

Wages $65,000Bad debt $1,395 ($38,450)Net income $53,605

balance sheet year 2Assets:

Cash $125,000

Accounts receivable $14,155

total assets $139,155

Equity:

Common stock $10,000

Retained earnings $129,155

total equity $139,155

statement of cash flows year 2Cash flows form operating activities:

Net income $53,605

adjustments:

Increase in accounts receivable ($5,605)

net cash from operating activities $48,000

Net cash increase $48,000

beginning cash balance $77,000

Ending cash balance $125,000

c) net realizable value of accounts receivable at year 1 = $8,550

net realizable value of accounts receivable at year 2 = $14,155

a. Recording the Year 1 and Year events in general journal form and posting to T-accounts for Leach Inc. are as follows:

General JournalYear 1:

Debit Cash $10,000

Credit Common stock $10,000

Debit Accounts Receivable $78,000

Credit Service Revenue $78,000

Debit Cash $36,000

Credit Service Revenue $36,000

Debit Cash $69,000

Credit Accounts Receivable $69,000

Debit Salaries Expense $38,000

Credit Cash $38,000

Adjustment:

Debit Bad Debts Expense $450

Credit Uncollectible Allowance $450

Year 2:

Debit Accounts Receivable $650

Credit Uncollectible Allowance $650

Debit Accounts Receivable $88,000

Credit Service Revenue $88,000

Debit Cash $32,000

Credit Service Revenue $32,000

Debit Cash $81,000

Credit Accounts Receivable $81,000

Debit Salaries Expense $65,000

Credit Cash $65,000

Adjustment:

Debit Bad Debts Expense $968

Credit Uncollectible Allowance $968

T-accounts:Year 1:

Cash AccountCommon stock $10,000

Service Revenue $36,000

Accounts Receivable $69,000

Salaries Expense $38,000

Balance $77,000

Uncollectible AllowanceBad debts Expense $450

Common Stock

Cash account $10,000

Accounts Receivable

Service Revenue $78,000

Cash $69,000

Balance $9,000

Service RevenueAccounts Receivable $78,000

Cash $36,000

Income Summary $114,000

Salaries ExpenseCash $38,000

Income Summary $38,000

Bad Debts Expense

Uncollectible Allowance $450

Income Summary $450

Year 2:

Cash AccountBalance $77,000

Service Revenue $32,000

Accounts Receivable $81,000

Salaries Expense $65,000

Balance $125,000

Uncollectible AllowanceBalance $450

Accounts Receivable $650

Bad debts expense $968

Balance $768

Common StockBalance $10,000

Accounts Receivable

Balance $9,000

Service Revenue $88,000

Uncollectible allowance $650

Cash $81,000

Balance $15,350

Service RevenueAccounts Receivable $88,000

Cash $32,000

Income Summary $120,000

Salaries ExpenseCash $65,000

Income Summary $65,000

Bad Debts Expense

Uncollectible Allowance $968

Income Summary $968

b. The preparation of the income statement, statement of changes in stockholders' equity, balance sheet, and statement of cash flows for Year 1 and Year 2 are as follows:

Leach Inc.

Income Statements for Year 1 and Year 2:Year 1 Year 2

Service Revenue $114,000 $120,000

Salaries Expense 38,000 $65,000

Bad Debts Expense 450 38,450 968 65,968

Net income $75,550 $54,032

Leach Inc.

Statements of Changes in Stockholders' Equity for Year 1 and Year 2:Year 1 Year 2

Beginning balance $10,000 $85,550

Net income 75,550 54,032

Ending balance $85,550 $139,582

Leach Inc.

Balance Sheets at Year 1 and Year 2:Year 1 Year 2

Assets:

Cash $77,000 $125,000

Accounts Receivable 9,000 15,350

Uncollectible Allowance (450) (768)

Total assets $85,550 $139,582

Equity:

Ending balance $85,550 $139,582

Leach Inc.

Statements of Cash Flows for Year 1 and 2:Operating Activities: Year 1 Year 2

Net income $75,550 $54,032

Changes in working capital:

Accounts receivable (8,550) (6,032)

Operating cash flows $67,000 $48,000

Financing Activities:

Common Stock $10,000 $0

Increase in cash flows $77,000 $48,000

c. The net realizable value of the accounts receivable at Year 1 is $8,550 ($9,000 - $450) and Year 2 is $14,582 ($15,350 - $768).

Data Analysis:Year 1:

Cash $10,000 Common stock $10,000

Accounts Receivable $78,000 Service Revenue $78,000

Cash $36,000 Service Revenue $36,000

Cash $69,000 Accounts Receivable $69,000

Salaries Expense $38,000 Cash $38,000

Adjustment:

Bad Debts Expense $450 Uncollectible Allowance $450

Year 2:

Uncollectible Allowance $650 Accounts Receivable $650

Accounts Receivable $88,000 Service Revenue $88,000

Cash $32,000 Service Revenue $32,000

Cash $81,000 Accounts Receivable $81,000

Salaries Expense $65,000 Cash $65,000

Adjustment:

Bad Debts Expense $968 Uncollectible Allowance $968

= $968 ($650 + $768 - $450)

$768 ($15,350 x 5%)

Learn more about preparing financial statements at https://brainly.com/question/735261

Cost of Goods Sold and Income Statement Schuch Company presents you with the following account balances taken from its December 31 adjusted trial balance:

Inventory, January 1 $40,000 Purchases returns $3,500

Selling expenses 35,000 Interest expense 4,000

Purchases 110,000 Sales discounts taken 2,000

Sales 280,000 Gain on sale of property (pretax) 7,000

General and administrative expenses 22,000 Freight-in 5,000

Additional data:

1. A physical count reveals an ending-inventory of $22,500 on December 31.

2. Twenty-five thousand shares of common stock have been outstanding the entire year.

3. The income tax rate is 30% on all items of income.

Required:

a. As a supporting document for Requirements 2 and 3, prepare a separate schedule for Schuch's cost of goods sold.

b. Prepare a 2013 multiple-step income statement.

c. Prepare a 2013 single-step income statement.

Answers

Answer:

Schuch Company

a) Schedule of Cost of Goods Sold

Inventory, January 1 $40,000

Purchases 110,000

Purchases returns -3,500

Freight-in 5,000

Cost of goods available for sale $151,500

less Inventory, December 31 22,500

Cost of goods sold $129,000

b) Multi-step Income Statement

For the year ended December 31, 2013:

Net Sales Revenue $278,000

Cost of Goods Sold 129,000

Gross profit $149,000

Expenses:

Selling expenses 35,000

General & admin exp. 22,000 57,000

Operating profit $92,000

Interest expense 4,000

Income after interest expense $88,000

Gain on sale of property (pretax) 7,000

Comprehensive income before tax $95,000

Income Tax (30%) 28,500

Net income $66,500

EPS = $2.66

c) Single-step Income Statement

For the year ended December 31, 2013:

Net Sales Revenue $278,000

Gain on sale of property (pretax) 7,000

Total revenue and gains $285,000

Cost of Goods Sold 129,000

Selling expenses 35,000

General & admin exp. 22,000

Interest expense 4,000

Total expenses $190,000

Income before taxes $95,000

Income Taxes (30%) 28,500

Net income $66,500

EPS = $2.66

Explanation:

a) Data and Calculations:

December 31 adjusted trial balance:

Inventory, January 1 $40,000

Purchases returns $3,500

Selling expenses 35,000

Interest expense 4,000

Purchases 110,000

Sales discounts taken 2,000

Sales 280,000

Gain on sale of property (pretax) 7,000

General and administrative expenses 22,000

Freight-in 5,000

Additional data:

Ending Inventory $22,500

Common Stock outstanding = 25,000

Income tax rate = 30%

Sales $ 280,000

Sales discounts taken 2,000

Net Sales Revenue $278,000

The following are selected account balances from Penske Company and Stanza Corporation as of December 31, 2021:

Penske Stanza

Revenues $(842,000 ) $(568,000 )

Cost of goods sold 299,700 142,000

Depreciation expense 207,000 304,000

Investment income Not given 0

Dividends declared 80,000 60,000

Retained earnings, 1/1/21 (668,000 ) (222,000 )

Current assets 572,000 566,000

Copyrights 1,076,000 449,500

Royalty agreements 604,000 1,180,000

Investment in Stanza Not given 0

Liabilities (546,000 ) (1,631,500 )

Common stock (600,000 )($20 par) (200,000 ) ($10 par)

Additional paid-in capital 150,000 80,000

On January 1, 2013, Penske acquired all of Stanza's outstanding stock for $680,000 fair value in cash and common stock. Penske also paid $10,000 in stock issuance costs. At the date of acquisition copyrights (with a six-year remaining life) have a $440,000 book value but a fair value of $560,000.

a. As of December 31,2013, what is the consolidated copyrights balance?

b. For the year ending December 31,2013, what is consolidated net income?

c. As of December 31,2013, what is the consolidated retained earnings balance?

d. As of December 31,2013, what is the consolidated balance to be reported for goodwill?

Answers

Answer:

a. $1,625,500

b. $437,300

c. $1,025,300

d. $58,000

Explanation:

a. As of 31, December 2013, what is the consolidated copy rights balance

b. For the year ending, December 31, 2013, what is consolidated net income

c. As of December 31, 2013, what is the consolidates retained earnings balance

d. As of December 31, 2013 what is the consolidated balance to be reported for Goodwill.

Please find attached detailed explanations to the above questions and answers.

Alice and Bob entered into a forward contract some time ago. Alice has the long position, while Bob has the short position. The forward contract will mature in three months and has a delivery price of $40. The current forward price for the contract is $42. The three-month risk-free interest rate (with continuous compounding) is 8%. What is the value Bob's position?

Answers

Answer:

$ - 1.96

Explanation:

After three months, Alice (long the contract) can buy the underlying by paying the delivery price of $40 which is $2 less than $42 the long position would have to pay if the contract was entered today.

DATA

Delivery price = $40

The three-month risk-free interest rate (with continuous compounding) =8%.

The current forward price = $42

Solution

So based on the present situation, Alice would be in $2 profit at the end of 3 months and Bob would be in $2 loss

Present value of Bob's loss (with continuous compounding) = 2\times e^{-0.08\times 0.25}

Present value of Bob's loss (with continuous compounding) = $1.96

The value of Bob's position is $ - 1.96

In 1998, the Russian government defaulted on its bonds. According to the open-economy macroeconomic model, this should have

Answers

Answer:

An increase in the net export and Russian interest rate.

Explanation: An open economy is an economy where all players which includes traders, investors and other stakeholders in the economy both within and outside the economy freely conduct their businesses and are controlled by market forces with minimal interference by Government agencies.

According to the open-economy macroeconomic model with the defaulting by the Russian government in 1998 will definitely lead to an increase in net export and an increase in Russian Interest rate.

A Corporation has two divisions: the South Division and the West Division. The corporation's net operating income is $26,900. The South Division's divisional segment margin is $42,800 and the West Division's divisional segment margin is $29,900. What is the amount of the common fixed expense not traceable to the individual divisions

Answers

Answer:

$45,800

Explanation:

Common fixed expense not traceable to the individual divisions = South division's divisional segment margin + west division's divisional segment - corporation's net operating income

Common fixed expense not traceable to the individual divisions = $42,800 + $29,900 - $26,900

Common fixed expense not traceable to the individual divisions = $45,800

The text presents five signs of organizational culture: mission statement, stories & language, physical layout, rules & policies, and rituals. Select an organization where you have worked or are familiar with and identify an example of each sign of organizational culture. How do you think each of these things conveyed the organizational culture to employees and customers/clients.

Answers

Answer:

Face book

mission statement: give people the power to build community and bring the world closer together.

physical layout: How Face book is constructed.

rules & policies: The employees are required to act honestly, lawfully, ethically and in favor of the company they represent.

rituals: Face book looks for innovation and breaking the status quo, and to do so Face book employees are invited to paint, create and decore their offices and public spaces with own made art.

Explanation:

Organizational culture is what we call the mix of core values and actions that make up an organization, it's mostly and widely used for companies but it also applies to schools, governments, non-profits, and any group of people working together towards a goal.

The mission statement is basically what the organization wants to achieve, or its dreamed goal.

Stories and language are the speech that the organization communicates to the audience or anyone interacting with it.

The physical layouts are the colors and buildings, apps, or any way of direct interaction that any person could have with the organization.

Rules and policies are what dictate the behavior of all the employees and people related to the organization.

And rituals are the activities that the organization does in order to reinforce the values and policies they try to live day by day, doing your own painting is one example of these rituals.

Key figures for Apple and Google follow.

$ millions Apple Google

Cash and equivalents. . . . . . . $20,484 $12,918

Accounts receivable, net. . . . . 15,754 14,137

Inventories. . . . . . . . . . . . 2,132 268

Retained earnings. . . . . . . . . 96,364 105,131

Cost of sales. . . . . . . . . . . 131,376 35,138

Revenues. . . . . . . . . . . . . . 215,639 90,272

Total assets. . . . . . . . . . . . 321,686 167,497

Required:

a. Compute common-size percents for each of the companies using the data provided.

b. If Google decided to pay a dividend, would retained earnings as a percent of total assets increase or decrease

Answers

Answer:

a. Common-size analysis Income statement figures expresses them as a percentage of Sales while for Balance sheet figures, entries are expressed as a percentage of Total Assets.

Cash and Cash Equivalents

Apple Google

= 20,484/321,686 = 6.37 % = 12,918/167,497 = 7.71%

Accounts Receivables

Apple Google

= 15,754/321,686 = 4.90 % = 14,137/167,497 = 8.44%

Inventories

Apple Google

= 2,132/321,686 = 0.66 % = 268/167,497 = 0.16%

Retained Earnings

Apple Google

= 96,364/321,686 = 29.96 % = 105,131/167,497 = 62.77%

Cost of Sales

Apple Google

= 131,376/215,639 = 60.92 % = 35,138/90,272 = 38.92%

Apple Google

Cash and equivalents 6.37% 7.71%

Accounts receivable, net 4.90% 8.44%

Inventories 0.66% 0.16%

Retained Earnings 29.96% 62.77%

Cost of Sales 60.92% 38.92%

Revenues 100% 100%

Total Assets 100% 100%

b. Dividends are paid from Retained Earnings so Retained earnings as a percent of total assets WILL DECREASE.

The number of people or subordinates that a manager effectively controls and directs is called the manager's span of:

Answers

Answer: Span of Control

Explanation:

A Manager's span of control refers to all the subordinates that report to that manager. The manager therefore effectively controls and directs them and as such is answerable for them.

Spans of Control are different depending on the type of company it is. A manager with a lot of people in their span of control is said to have a Wide span of control and the reverse is a Narrow Span of control.

A very important part of management is determining the largest number of subordinates that can be in a span of control without overwhelming the manager.

Chance company had two operating divisions, one manufacturing farm equipment and other office supplies. Both divisions are considered separate components as defined by generally accepted accounting principles. The farm equipment component had been unprofitable, and on Sept. 1, 2016, the company adopted a plan to sell the assets of the division.

The actual sale was completed on Dec. 15, 2016, at the price of $600,000. The book value of the division's assets was $1,000,000, resulting in a before-tax loss of $400,000 on the sale. The division incurred a before-tax operating loss from operations of $130,000 from the beginning of the year through Dec. 15. The income tax rate is 40%. Chances after-tax income from its continuing operations is $350,000.

Required:

Prepare an income statement for 2016 beginning with income from continuing operations. Include appropriate EPS disclosures assuming that 100,000 shares of common stock were outstanding throughout the year.

Answers

Answer:

-21,000

Explanation:

We can calculate the net income by Adding/deducting the gain/loss on the discontinued operations from the gain/loss of the continuing operations.

INCOME STATEMENT

Income from continuing Operations $350,000

Discontinued Operations

Loss from discontinued operations(w) -530,000

Income tax benefit $159,000

(400,000+130,000) x 30%

Net Income -21,000

Earning per share

Continuing Operations $3.5

(350,000/100,000)

Discontinued Operations -$5.3

(-530,000/100,000)

Net Income -$1.8

Working

Sale value of the segment $600,000

Book value of the segment ($1,000,000)

loss on sale of segment -$400,000

Loss from the Operations of the segment -$130,000

Loss on discontinued operation -$530,000

The December 31, 2018, adjusted trial balance for Fightin' Blue Hens Corporation is presented below.

Accounts Debit Credit

Cash $12,000

Accounts Receivable 150,000

Prepaid Rent 6,000

Supplies 30,000

Equipment 400,000

Accumulated Depreciation $135,000

Accounts Payable 12,000

Salaries Payable 11,000

Interest Payable 5,000

Notes Payable (due in two years) 40,000

Common Stock 300,000

Retained Earnings 60,000

Service Revenue 500,000

Salaries Expense 400,000

Rent Expense 20,000

Depreciation Expense 40,000

Interest Expense 5,000

Totals $1,063,000 $1,063,000

Accounts Debit Credit

Service Revenue 500,000

Salaries Expense 400,000

Rent Expense 20,000

Depreciation Expense 40,000

Interest Expense 5,000

Total $1,063,000 $1,063,000

Required:

1. Prepare an income statement for the year ended December 31, 2021.

2. Prepare a statement of stockholders' equity for the year ended December 31, 2021, assuming no common stock was issued during 2021.

3. Prepare a classified balance sheet as of December 31, 2021.

Answers

Answer:

Please see answers below

Explanation:

1. Prepare an income statement for the year ended, December 31, 2021

Fightin' Blue Hems Corporation, Income statement for the year ended, December 31, 2021.

Details

$

Service revenue

500,000

Salaries expense

400,000)

Rent expense

20,000)

Depreciation expense

40,000)

Interest expense

5,000)

Earnings for the year

35,000

2. Prepare a statement of stockholder's equity for the year ended, 31, December, 2021

Fightin' Blue Hens Corporation statement of stockholder equity for the year ended , December 31, 2021.

Details

$

Common stock

300,000

Retained earnings

60,000

Earnings for the year

35,000

Stockholder equity

395,000

3. Prepare a classified balance sheet as at 31, December

Fightin' Blue Hens Corporation, classified balance sheet for the hear ends, December 31, 2021.

Details

$

Fixed assets

Equipment

400,000

Accumulated depreciation

135,000

Net fixed assets

265,000

Current assets

Cash

12,000

Accounts receivables

150,000

Prepaid rent

6,000

Supplies

30,000

Total current assets

198,000

Current liabilities

Accounts payable

($12,000)

Salaries payable

(11,000)

Interest payable

(5,000)

Working capital

170,000

Long term liabilities

Notes payable (due in two years)

(40,000)

Net total assets

395,000

Financed by;

Common stock

300,000

Retained earnings

60,000

Earnings for the year

35,000

Stockholder equity

395,000

The revenues budget identifies: a. expected cash flows for each product b. actual sales from last year for each product c. the expected level of sales for the company d. the variance of sales from actual for each product

Answers

Answer:

c. the expected level of sales for the company

Explanation:

Revenue/Sales Budget is the first budget to be prepared by most companies because most businesses are sales led.

This Budget shows, the expected level of sales for the company.

Cooperative San José of southern Sonora state in Mexico makes a unique syrup using cane sugar and local herbs. The syrup is sold in small bottles and is prized as a flavoring for drinks and for use in desserts. The bottles are sold for $12 each. The first stage in the production process is carried out in the Mixing Department, which removes foreign matter from the raw materials and mixes them in the proper proportions in large vats. The company uses the weighted-average method in its process costing system.

A hastily prepared report for the Mixing Department for April appears below:

Units to be accounted for:

Work in process, April 1 (materials 90% complete; conversion 80% complete) 5,700

Started into production 34,100

Total units to be accounted for 39,800

Units accounted for as follows:

Transferred to next department 29,400

Work in process, April 30 (materials 70% complete; conversion 50% complete) 10,400

Total units accounted for 39,800

Cost Reconciliation Cost to be accounted for:

Work in process, April 1 $15,276

Cost added during the month 96,248

Total cost to be accounted for $111,524

Cost accounted for as follows:

Work in process, April 30 $20,384

Transferred to next department 91,140

Total cost accounted for $111,524

Required:

a. What were the Mixing Department's equivalent units of production for materials and conversion for April?

b. What were the Mixing Department's cost per equivalent unit for materials and conversion for April? The beginning inventory consisted of the following costs: materials, $10,545; and conversion cost, $4,731. The costs added during the month consisted of: materials, $64,649; and conversion cost, $31,599.

c. How many of the units transferred out of the Mixing Department in April were started and completed during that month?

d. The manager of the Mixing Department stated, "Materials prices jumped from about $1.65 per unit in March to $2.15 per unit in April, but due to good cost control I was able to hold our materials cost to less than $2.15 per unit for the month." Should this manager be rewarded for good cost control?

Answers

Answer:

a. EU:

materials = 29,400 + 7,280 = 36,680

conversion = 29,400 + 5,200 = 34,600

b. cost per EU:

materials = $75,194 / 36,680 = $2.05

conversion = $36,330 / 34,600 = $1.05

c. units started and completed during April = 23,700

d. no, he didn't do anything, When a company uses the weighted average process costing method, the cost of beginning WIP is used to determine the cost per equivalent unit. On the other hand, FIFO process costing method doesn't, it only considers costs incurred during the month to calculate cost per equivalent unit.

Explanation:

beginning WIP 5,700 $15,276

materials, $10,545

conversion cost, $4,731

units started 34,100

costs added during the month = $96,248

materials, $64,649

conversion cost, $31,599

units transferred out 29,400 $91,140

ending WIP 10,400 $20,384

materials 70% = 7,280 EU

conversion 50% = 5,200 EU

EU:

materials = 29,400 + 7,280 = 36,680

conversion = 29,400 + 5,200 = 34,600

total cost for materials = $64,649 + $10,545 = $75,194

total cost for conversion = $31,599 + $4,731 = $36,330

cost per EU:

materials = $75,194 / 36,680 = $2.05

conversion = $36,330 / 34,600 = $1.05

units started and completed during April = 29,400 - 5,700 = 23,700

Presented below is information from Headland Computers Incorporated.

July 1 Sold $22,600 of computers to Robertson Company with terms 3/15, n/60. Headland uses the gross method to record cash discounts. Headland estimates allowances of $1,334 will be honored on these sales.

10 Headland received payment from Robertson for the full amount owed from the July transactions.

17 Sold $256,100 in computers and peripherals to The Clark Store with terms of 2/10, n/30.

30 The Clark Store paid Headland for its purchase of July 17.

Answers

Answer:

July 1

Dr Accounts receivable $22,600

Cr Cash $22,600

Dr Sales returns and allowances $1,334

Cr Allowances for Sales returns and allowances $1,334

July 10

Dr Cash $21,922

Dr Sales Discount $678

Cr Accounts Receivable $22,600

July 17

Dr Accounts receivable $256,100

Cr Sales revenue $256,100

July 30

Dr Cash $256,100

Cr Accounts receivable $256,100

Explanation:

Preparation of Journal entry

July 1

Dr Accounts receivable $22,600

Cr Cash $22,600

Dr Sales returns and allowances $1,334

Cr Allowances for Sales returns and allowances $1,334

July 10

Dr Cash $21,922

(97%×$22,600)

Dr Sales Discount $678

(3%×$22,600)

Cr Accounts Receivable $22,600

($21,922+$678)

July 17

Dr Accounts receivable $256,100

Cr Sales revenue $256,100

July 30

Dr Cash $256,100

Cr Accounts receivable $256,100

In 2009, an 1893 Morgan silver dollar sold for $6,450. Required: What was the rate of return on this investment? (Do not include the percent sign (%). Enter rounded answer as directed, but do not use the rounded numbers in intermediate calculations. Round your answer to 2 decimal places (e.g., 32.16).)

Answers

Answer: 7.86%

Explanation:

Using the Future Value formula;

= Amount * ( 1 + r)^n

The question is looking for the rate so making that the subject would be;

Assuming the car was $1 in 1893,

And n = 2009 - 1893 = 116 years

FV = Amount * ( 1 + r)^n

( 1 + r)^n = FV/ Amount

1 ^n + r^n = FV / Amount

r = n√((FV/ Amount) / 1^n)

r = n√(FV/ Amount)

r = 116√(6,450/ 1)

= 1.07855

Subtract 1 for the percentage;

= 1.07855 - 1

= 7.86%

Mattola Company is giving each of its employees a holiday bonus of $200 on December 13, 20-- (a nonpayday). The company wants each employee's check to be $200. The supplemental tax percent is used.

Nobody has capped for OASDI prior to the bonus check.

a. What will be the gross amount of each bonus if each employee pays a state income tax of 2.8% (besides the other payroll taxes)? You may need to add one penny to the gross so that net bonus exactly equals $200. Round your calculations and final answers to the nearest cent.

b. What would the net amount of each bonus check be if the company did not gross-up the bonus? Round your intermediary calculations to the nearest cent.

Answers

Answer:

a. Gross amount of each bonus = $309.84

b. Net amount of each bonus = $129.10

Explanation:

Since the supplemental tax percent is used, the following are the relevant tax rates to be applied in the calculations:

STP = Supplemental tax percent = 25%

FICASO = Federal Insurance Contributions Act (FICA) social security tax = 6.2%

FICAM = Federal Insurance Contributions Act (FICA) Medicare tax = 1.45%.

SIT = State income tax = 2.8%

We therefore proceed as follows:

a. What will be the gross amount of each bonus if each employee pays a state income tax of 2.8% (besides the other payroll taxes)? You may need to add one penny to the gross so that net bonus exactly equals $200. Round your calculations and final answers to the nearest cent.

Given the tax rates above, the following formula is used to calculate the gross amount of each bonus:

Gross amount of each bonus = Holiday bonus amount / (100% - STP - FICASO - FICAM - SIT) …… (1)

Substituting the relevant values into equation (1), we have:

Gross amount of each bonus = $200/ (100% - 25% - 6.20% - 1.45% - 2.8%)

Gross amount of each bonus = $200 / 64.55%

Gross amount of each bonus = $309.837335398916

To the nearest cent which implies to two decimal places, we have:

Gross amount of each bonus = $309.84

b. What would the net amount of each bonus check be if the company did not gross-up the bonus? Round your intermediary calculations to the nearest cent.

The net amount of each bonus can be calculated using the following formula:

Net amount of each bonus = Holiday bonus amount * (100% - STP - FICASO - FICAM - SIT) …… (2)

Substituting the relevant values into equation (2), we have:

Net amount of each bonus = $200 * (100% - 25% - 6.20% - 1.45% - 2.8%)

Net amount of each bonus = $200 * 64.55%

Net amount of each bonus = $129.10

Blago Wholesale Company began operations on January 1, 2017, and uses the average cost method in costing its inventory. Management is contemplating a change to the FIFO method in 2018 and is interested in determining how such a change will affect net income. Accordingly, the following information has been developed:

2017 2018

Final inventory:

Average cost $150,000 $255,000

FIFO 160,000 270,000

Condensed income statements for Blago Wholesale appear below:

2017 2018

Sales $1,000,000 $1,200,000

Cost of goods sold 600,000 720,000

Gross profit 400,000 480,000

Selling, general, and administrative 250,000 275,000

Net income $150,000 $205,000

Required:

Based on this information, what would 2018 net income be after the change to the FIFO method?

Answers

Answer:

Blago Wholesale Company

New Net income for 2018 = $220,000

Explanation:

Data and Calculations:

Final inventory: 2017 2018

Average cost $150,000 $255,000

FIFO 160,000 270,000

Difference $10,000 $15,000

2017 2018

Sales $1,000,000 $1,200,000

Cost of goods sold 600,000 720,000

Gross profit 400,000 480,000

Selling, general, and

administrative 250,000 275,000

Net income $150,000 $205,000

2018 Net Income after the change to the FIFO method:

Cost of goods sold (weighted average) 720,000

less adjustment for change of method 15,000

Adjusted cost of goods sold 705,000

Income Statement after the change

Sales $1,200,000

Cost of goods sold 705,000

Gross profit 495,000

Selling, general, and

administrative 275,000

Net income $220,000

BMW’s vehicle-assembly facility in South Carolina represents a direct investment inside the United States by the German manufacturer. This facility is an example of:

Answers

Answer:

Foreign direct investment.

Explanation:

BMW’s vehicle-assembly facility in South Carolina represents a direct investment inside the United States by the German manufacturer. This facility is an example of foreign direct investment.

A foreign direct investment (FDI) can be defined as an investment made by an individual or business entity (investor) into an investment market (industry) located in another country. The investor here, shares a different country of origin from the country where his investment is located.

In a foreign direct investment (FDI), an investor must establish his business, factory and operations in a foreign country or acquire assets in a business that is being operated in a foreign country.

Additionally, foreign direct investment (FDI) are categorized into three (3) main types and these are;

1. Vertical FDI: it involves establishing a different business that is however similar to the main business owned by the investor.

2. Horizontal FDI: it involves establishing the same type of business in a foreign country as owned in the investor's country.

3. Conglomerate FDI: it involves establishing a business that is completely different in another (foreign) country.

Presented below are condensed financial statements adapted from those of two actual companies competing as the primary players in a specialty area of the food manufacturing and distribution industry. ($ in millions, except per share amounts.)

Balance Sheets

Metropolitan Republic

Assets $ 179.3 $ 37.1

Cash

Accounts receivable (net) 422.7 325.0

Short-term investments — 4.7

Inventories 466.4 635.2

Prepaid expenses and other current assets134.6 476.7

Current assets $ 1,203.0 1,478.7

Property, plant, and equipment (net) 2,608.2 2,064.6

Intangibles and other assets 210.3 464.7

Total assets $ 4,021.5 $4,008.0

Liabilities and Shareholders’ Equity

Accounts payable $ 467.9 691.2

Short-term notes 227.1 557.4

Accruals and other current liabilities 585.2 538.5

Current liabilities $ 1,280.2 1,787.1

Long-term debt 535.6 542.3

Deferred tax liability 384.6 610.7

Other long-term liabilities 104.0 95.1

Total liabilities $ 2,304.4 3,035.2

Common stock (par and additional paid-in capital)

144.9 335.0

Retained earnings 2,476.9 1,601.9

Less: treasury stock (904.7) (964.1)

Total liabilities and shareholders’ equity $

4,021.5 4,008.0

Income Statements

Net sales 5,698.0 7,768.2

Cost of goods sold (2,909.0) (4,481.7)

Gross profit $ 2,789.0 3,286.5

Operating expenses (1,743.7 ) (2,539.2)

Interest expense (56.8) (46.6)

Income before taxes $ 988.5 700.7

Tax expense (394.7) (276.1)

Net income 593.8 424.6

Net income per share $ 2.40 6.50

Note: Because comparative statements are not provided you should use year-end balances in place of average balances as appropriate.

Required:

Calculate the rate of return on assets for the following companies

Calculate the return on assets for both companies.

Calculate the Rate of return on shareholders’ equity for the following companies

Calculate the equity multiplier for the following companies.

Calculate the acid-test ratio and current ratio for the following companies.

Calculate the receivables and inventory turnover ratios the following companies.

Calculate the times interest earned ratio for the following companies.

Answers

Answer and Explanation:

We refer to balance sheet figures for each company stated above to retrieve figures for our calculations and use the following formulas for calculations:

For return on assets= net imcome/total assets

For rate of return on shareholders equity =net income/equity

For equity multiplier= total assets/ total equity

For acid-test ratio=liquid assets/current liabilities

For current ratio =current assets/current liabilities

For receivables = credit sales /acct receivables and inventory turnover ratios=cost of goods/inventory

For times interest earned ratio=ebit/interest expenses

What will be the nominal rate of return on a perpetual preferred stock with a $100 par value, a stated dividend of 8% of par, and a current market price of (a) $62, (b) $81, (c) $97, and (d) $136

Answers

Answer and Explanation:

The computation of the risk premium is shown below:-

Rate of return = Dividend ÷ Current market price of preferred stock

The dividend should be

= $100 × 8%

= $8

a Rate of return = $8 ÷ $62

= 12.90%

b. Rate of return = $8 ÷ $81

= 9.88%

c. Rate of return = $8 ÷ $97

= 8.25%

d. Rate of return = $8 ÷ $136

= 5.88%

Wilson Products uses standard costing. It allocates manufacturing overhead (both variable and fixed) to products on the basis of standard direct manufacturing labor-hours (DLH). Wilson Products develops its manufacturing overhead rate from the current annual budget. The manufacturing overhead budget for 2014 is based on budgeted output of 672,000 units, requiring 3,360,000 DLH. The company is able to schedule production uniformly throughout the year.

A total of 72,000 output units requiring 321,000 DLH was produced during May 2014. Manufacturing overhead (MOH) costs incurred for May amounted to $ 355,800. The actual costs, compared with the annual budget and 1/12 of the annual budget, are as follows:

Calculate the following amounts for Wilson Products for May 2014:

Total Amount Per Output Unit Per DLH Input Unit Monthly MOH Budget May 2017 Actual MOH Costs for May 2017

Variable MOH

Indirect manufacturing labor $1,008,000 $1.50 $0.30 $84,000 $84,000

Supplies 672,000 1.00 0.2 56,000 117,000

Fixed MOH

Supervision 571,200 0.85 0.17 47,600 41,000

Utilities 369,600 0.55 0.11 30,800 55,000

Depreciation 705,600 1.05 0.21 58,800 88,800

Total $33,26,400 $4.95 $0.99 $277,200 $355,800

Required:

a. Total manufacturing overhead costs allocated.

b. Variable manufacturing overhead spending variance.

c. Fixed manufacturing overhead spending variance.

d. Variable manufacturing overhead efficiency variance.

e. Production-volume variance Be sure to identify each variance as favorable (F) or unfavorable(U).

Answers

Answer:

Please see attached solution

Explanation:

a. Total manufacturing overhead costs allocated $356,400

b. Variable manufacturing overhead spending variance $40,500U

c. Fixed manufacturing overhead spending variance $17,600U

d. Variable manufacturing overhead efficiency variance $19,500F

e. Production volume variance $39,200F

Please find attached detailed solution to the above questions

Which best describes the role that government and business play in investments?

O They both use taxes to support a country's growth.

They both invest money to earn a profit.

They both receive capital to use for growth.

They both act as angel investors for start-ups.

Answers

Answer:

They both receive capital to use for growth.

Explanation:

The government received the capital in the form of tax that being paid by the citizens. After collecting the tax income, the government allocated it to make a couple of investments such as building the country's infrastructure, providing aid for people to pursue education, and investing in scientific research/development.

Business on the other hand could receive their capital from either reallocating their profit or receiving capital injection from the investors. They use the capital for growth by reinvesting it to increase the scope of their business operation or putting it under investment accounts.

Statement that best describes the role that government and business play in investments is They both receive capital to use for growth

What is an investment?Investment can be regarded as the input that is been put into some business in order to generate revenue.

however, this also applies to the government because they use the public funds as investment for the betterment of the economy and the public.

Learn more about investments at;

https://brainly.com/question/200850

Last month Empire Company had a $35,280 profit on sales of $287,000. Fixed costs are $68,040 a month. By how much would sales be able to decrease for Empire to still break even

Answers

Answer:

sales might decrease by $287,000 - $189,000 = $98,000 and the company will still break even

Explanation:

gross profit = net income + fixed costs = $35,280 + $68,040 = $103,320

COGS = total sales - gross profit = $287,000 - $103,320 = $183,680

contribution margin ratio = $103,320 / $287,000 = 36%

break even point in $ = $68,040 / 36% = $189,000

sales might decrease by $287,000 - $189,000 = $98,000 and the company will still break even